Despite market uncertainty and a volatile geopolitical climate, in Q1 this year, major carriers recorded a combined Ebit of $5.89 billion, according to research by maritime consultancy Sea-Intelligence.

This is only lower than Q1 in the 2021-2023 pandemic period.

As market disruptions continued in Q2, with shifting volumes and consistent downward pressure on freight rates, the same major lines recorded a combined Ebit of $2.73bn for the period.

“This was lower than Q2 in not only 2021-2024, but also only slightly higher than in 2020. This meant that, while still profitable, 2025-Q2 was relatively less profitable than most of the recent years,” said CEO Alan Murphy.

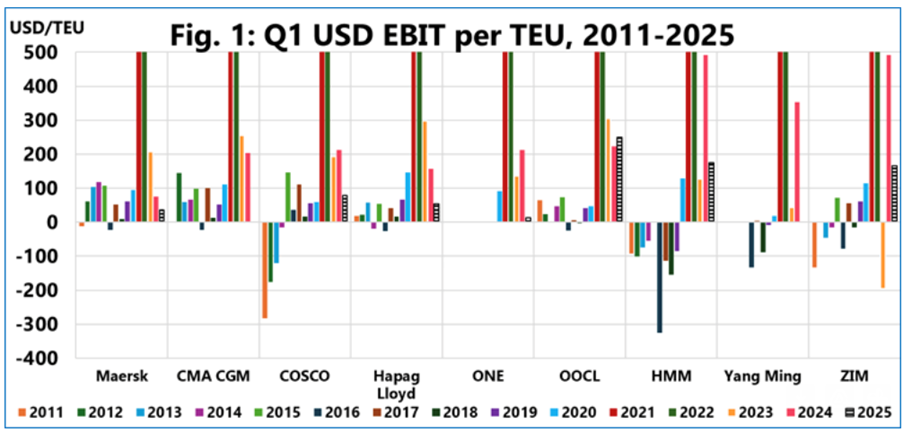

To show operational profitability in container shipping, the maritime consultancy uses the Ebit/TEU figure.

Figure 1 shows this metric for the major lines for each Q2 since 2011. “We are missing a 2025-Q2 figure for Yang Ming as they have not published their volumes for this period, and CMA CGM, as they have not published a publicly available Ebit for this period. Furthermore, the y-axis is cut off at 500 USD/TEU so that current figures are not obscured by the pandemic highs,” he added.

All major lines reported positive Ebit/TEU, ranging from 12 USD/TEU (ONE) to 249 USD/TEU (OOCL). There were three more shipping lines with an Ebit/TEU of under 100 USD/TEU: Maersk (35 USD/TEU), Hapag-Lloyd (53 USD/TEU), and COSCO (79 USD/TEU), while there were two with an Ebit/TEU of 100-200 USD/TEU: HMM (176 USD/TEU) and ZIM (167 USD/TEU).

“The 2025-Q2 financial reports also showed a divided Transpacific and Asia-Europe market. The Asia-Europe trade recorded strong volume growth, with three of the six shipping lines that report on Asia-Europe volumes recording double-digit year-on-year increases. Conversely, the transpacific trade experienced widespread volume contractions,” he added.