Global disruption is no longer a distant risk – it is actively reshaping the operating environment for South Africa and the broader sub-Saharan region, says Dr Juanita Maree, chief executive officer of the South African Association of Freight Forwarders (Saaff).

In a LinkedIn post about the conflict in the Middle East and the subsequent Strait of Hormuz, she emphasises that for local businesses “this is not a moment for passive observation. It is a time for disciplined response – tight cost control, strengthened fuel and freight strategies, and heightened vigilance across supply networks.”

According to Maree, supply chain disruptions through the important waterway linking the Persian Gulf with the Gulf of Oman, “confirm a prolonged period of constrained maritime flow, rising energy costs, and increasing logistics complexity”.

“What began as a geopolitical shock is now translating into a tangible world economic tsunami: elevated fuel inflation, stressed supply chains, and shifting regional trade dynamics.”

Despite recent pronouncements around March 31 by President Donald Trump that the US had achieved its military objectives and was ready to exit the theatre of war within the next two to three weeks, “the latest view is that the war remains active”.

This is according to an assessment by Saaff’s head of Research and Industry Intelligence, Dr Jacob van Rensburg.

Done in conjunction with the Durban Chamber of Commerce (DCC), the assessment adds that “indirect talks are still being reported, but there is no confirmed durable ceasefire”.

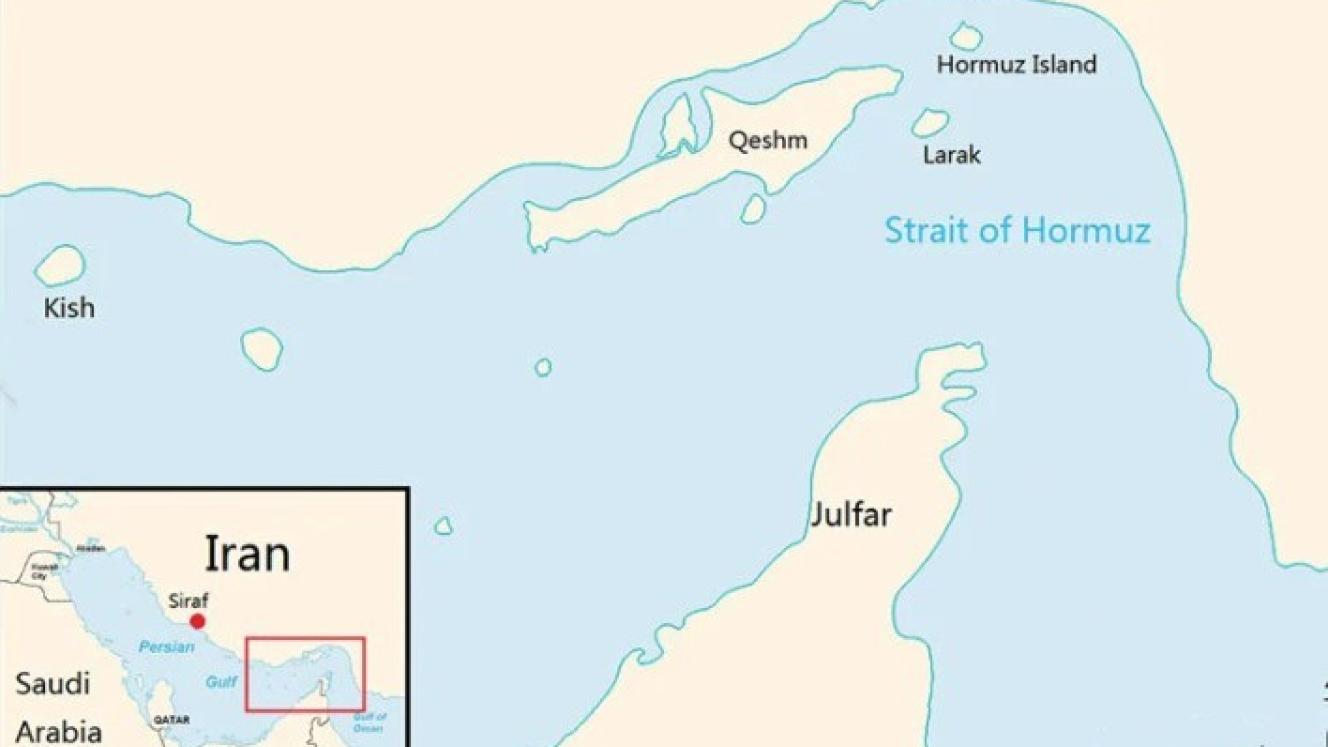

“The Strait of Hormuz is still effectively shut to normal commercial traffic, with only a limited trickle of vessels moving under tightly controlled conditions.”

Although Iran has formulated a de-facto payment and vetting regime for flag-friendly vessels to transit through Strait, hugging its coastline and skirting Larak Island near the coast of Qeshm, news agencies such as Reuters and Associated Press say there’s little if any relief for some lines stuck in the Persian Gulf.

Hamburg line Hapag-Lloyd, a Gemini Cooperation vessel-sharing partner of Maersk, is one of the carriers still waiting to exit the chokepoint area.

Threatened by the risk of vessel attack by the Islamic Revolutionary Guard Corps roaming Hormuz waters, the line’s German ownership has not made passage safer despite Germany’s expressed unwillingness, as a Nato member, to get involved in a war started by the US and Israel.

Coming ahead of this week’s fuel price increase in South Africa, the assessment says one of the most concerning aspects of the conflict’s local impact is that the Reserve Bank has projected second-quarter fuel inflation above 18%.

Looking wider, the Saaff assessment says: “Across sub-Saharan Africa, the effects are now showing up more clearly in real operations.”

“Reuters reports fuel stress in multiple African markets, including shortages or rationing pressure in Mauritius, Kenya, Uganda, Somalia, and South Sudan. In West Africa, Dangote’s refinery has gained leverage as disrupted Middle East flows dry up cheaper imports, and Reuters says Nigeria’s clean-product exports have risen sharply in March, increasing its importance as an alternative regional supplier.

“On shipping and logistics, the main risk has worsened rather than eased. Reuters says prolonged Hormuz disruption could remove 13-14 million barrels per day from global supply, while oil options markets are increasingly pricing a tail risk of much higher prices if the blockage lasts.

“At the same time, Reuters and AP both indicate that some traffic is being rerouted or negotiated through, but this is not normalisation; it is a constrained, higher-cost workaround.”

For South Africa and the Sub-Saharan (SSA) market, “The most relevant near-term risk mix is now: fuel-price passthrough into road freight and public transport; higher insurance, bunker, and freight costs; tighter availability of petrochemical inputs such as plastics; higher exposure to diesel theft, tanker crime, and stockpiling behaviour; and a stronger chance of intermittent shortages in countries with weaker buffers.”

Reuters also reported that rerouting around the Cape was benefiting some African bunkering hubs, so there is a partial upside for Southern African maritime services even as inland fuel and logistics costs rise, the assessment continues.

It stresses that the biggest changes are fourfold.

“First, the market now has stronger evidence that Hormuz disruption is persisting, not just as ad hoc interference but through a more organised Iranian control regime. Second, the South African macro impact has hardened: the SA Reserve Bank has formally signalled higher fuel inflation and greater caution on rates.

“Third, African spillovers are no longer mostly anticipatory; Reuters is now reporting concrete fuel stress across several African states. Fourth, maritime risk has broadened, because Reuters reports that the Houthis are signalling readiness to join if needed, which raises the risk beyond Hormuz to the Bab al-Mandab/Red Sea system as well.”

So where does it leave SA and the SSA?

According to Van Rensburg and the DCC’s assessment, the outlook for the wider region remains negative.

By Thursday morning there was no confirmed normalisation, Hormuz disruption continued, there was elevated fuel-inflation risk and growing logistics fragility.

“Businesses should prioritise cost containment, freight consolidation, tighter fuel-security controls, and close monitoring for sudden shifts in shipping access and regional fuel supply,” the assessment said.