As shippers battle the sky-high rates that have characterised the industry during the pandemic, carriers have blamed escalating operating costs for the increases.

But what are the underlying costs of operating liner services - and how much have these costs actually increased?

“This provides one of the anchor points in assessing where the baseline rate level may settle once we get through the present rate normalisation,” says maritime consultancy Sea-Intelligence.

“While it would be ideal to analyse costs across multiple carriers, few carriers provide detailed cost data,” says CEO Alan Murphy.

Hapag-Lloyd has, however, proved to be the exception, providing granular detail on a systematic basis, and with several years of history.

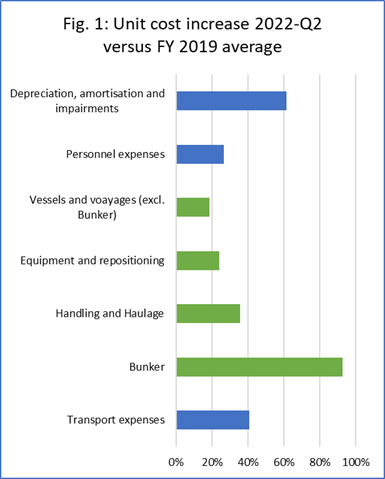

Based on the assumption that Hapag-Lloyd is representative of the market, there are three major cost categories - transport expenses, personnel expenses, and depreciation, amortisation and impairments.

Transport expenses are subdivided into bunker, handling and haulage, equipment and repositioning, vessels and voyages (excluding bunker), and expenses for pending voyages. This is an exceedingly small element, says Murphy, and will not be analysed here.

Figure 1 shows a comparative overview of the increases in each of these cost elements. The unit cost is calculated across transported volumes in that quarter. The blue bars are the three main cost categories, and the green bars are the subcomponents of transport expenses.

Bunker costs are seen here to have experienced the largest relative cost increase compared to 2019. “When we account for the relative share, the cost increase in handling and haulage is accountable for 37% of the unit cost increase, followed by bunker fuel which is accountable for 30%. This means that two-thirds of the inflationary pressure is related to fuel, handling and haulage. This is also a key pointer as to where the carriers are likely to focus in the months ahead, as the ongoing market downturn will force carriers to focus on cost reductions,” says Murphy.